In a word: Yes, prepaid insurance is an asset. Anything that is owned by a company and has a future value that can be measured in money is considered an asset. This includes cash, accounts receivable, inventory, real estate, buildings, equipment, supplies, vehicles – and prepaid expenses, such as insurance premiums and prepaid rent.

When an asset is expected to be consumed or used in the company’s regular business operations within the accounting year, it is recorded as a current asset. Current assets, sometimes also referred to as current accounts, are shown on the company’s balance sheet.

What is prepaid insurance?

Insurance is typically a prepaid expense, with the full premium paid in advance for a policy that covers the next 12 months of coverage. This is often the case for health, life, hazard, automotive, liability and other forms of coverage required by a business.

When a business policyholder pays the premium in advance, the total amount is shown as a current asset and is carried as an asset until the coverage is used. When the coverage is applied for one month, that amount is expensed on the income statement, and it is no longer shown as an asset.

Learn More About Business Insurance

An Exception to the Current Asset Rule

Rarely, an insurance policy will extend coverage beyond the 12-month accounting period following payment of the initial premium. In such a case, the portion of insurance prepaid in the prior year and used in the following year is a long-term asset.

Why not just record an expense?

When a company uses the accrual method of accounting, the concept of prepaid (including rents, insurance and certain other expenses) allows the accounting process to match the payment for expenses with the periods in which they are actually consumed.

This enables the most accurate reflection of assets in the short term, as well as profit. The concept of prepaid is not used in the cash method of accounting, which is most often used by small businesses.

Accounting Steps to Record Prepaid Insurance

- Charge the invoice from the insurance company to the prepaid expenses account.

- Record the expense in the reconciliation worksheet used for prepaid expenses.

- Determine the number of periods over which the prepaid amount will be amortized.

- Indicate the amount of amortization to be charged in each period.

- In each period, make an adjusting journal entry amortizing that amount as an insurance expense on the income statement.

- When fully amortized, match the worksheet total to the prepaid expense account balance.

An Example of Prepaid Insurance Accounting

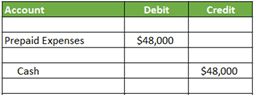

A small company has an insurance contract under which the total premium of $48,000 must be paid in advance for 12 months of coverage under a general liability insurance policy. In this example, the journal entry’s initial expense would be recorded as a debit to Prepaid Expenses and a credit to Cash.

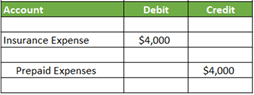

The company then amortizes the prepaid expense account with journal entries at the end of each period which will, by the end of the year, charge the full amount of the prepaid expenditure to the insurance expense account. Each journal entry requires a debit to Insurance Expenses and a credit to Prepaid Expenses.

How is prepaid insurance reflected on financial statements?

A prepaid insurance contract is recorded initially as an asset. Adjusting journal entries are then needed each month so that (1) the current month’s expense is recorded on each month’s income statement, and (2) the unexpired amount of the prepaid insurance is reduced each month in the asset account.

The monthly adjusting journal entries will be shown on both the company’s income statement (as a $4,000 expense) and on the company’s balance sheet as a $4,000 reduction to the prepaid expense asset account.

Key Takeaways

- Prepaid insurance is a current asset if coverage is used within one year of payment.

- Should coverage extend beyond 12 months, that portion can be a long-term asset.

- The asset is converted to an expense for the period in which the prepaid is used.

- Prepaids are tracked in the accrual method of accounting, but not the cash method.

- When insurance is prepaid, the accountant sets up an amortization worksheet.

- Initially, the total insurance premium paid is a debit to prepaid expense and a credit to cash.

- As each monthly portion of the prepaid asset amortizes or expires, it is expensed on the income statement, and the balance sheet is adjusted by recording a debit to insurance expense and a credit to prepaid expenses in an amount equal to the monthly portion until it has been fully realized and amortized.

Want to learn more about prepaid insurance to determine if it’s right for you? Higginbotham can help. Talk to an insurance and risk management specialist today.